Meaning of Single-Entry System

Single entry system is a system of Book-Keeping that records only cash and personal aspects of the transactions. This is the reason we call it an Incomplete system also.

In this system, we maintain Cash Book and personal accounts of debtors and creditors. Real and nominal Accounts are not there.

Features of Single-Entry System

- It is an unsystematic method of recording transactions.

- It generally, records for cash transactions and personal accounts only.

- We do not record Personal transactions of owners, in the cash book.

- There is lack of uniformity. Every business organisations can maintain records in their own way.

- Calculation of profit or loss depends on original vouchers only.

- We can find Only estimated profit or loss for the year.

- It shows Only the estimated financial position of business.

Limitations of Single-Entry System

The limitations of incomplete records are as follows:

- We cannot prepare Trial balance to check the arithmetical accuracy of accounts.

- Correct calculation of Net Profit/Loss of business also is out of question.

- Analysis of profitability, liquidity and solvency of the business cannot be done.

- There is difficulty in filing an insurance claim as exact loss cannot be calculated.

- Single Entry System not acceptable to the income tax authorities.

- Large business enterprises cannot use this system.

It is due to disadvantages that Double Entry System came into existence.

Preparation of Financial Statements:

Following statements are prepared to show the financial position and to calculate profit earned during the accounting year.

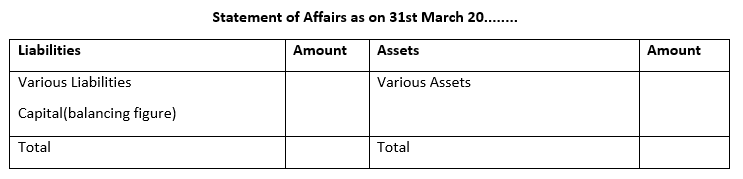

- Opening and Closing Statements of Affairs:

A statement prepared on the basis of the estimated balances of various assets and liabilities on a particular date is called Statements of Affairs.

Statement of Affairs are prepared at the beginning and at the end of the accounting year to calculate the Capital on the two dates and to show the financial position.

Proforma of Statements of Affairs

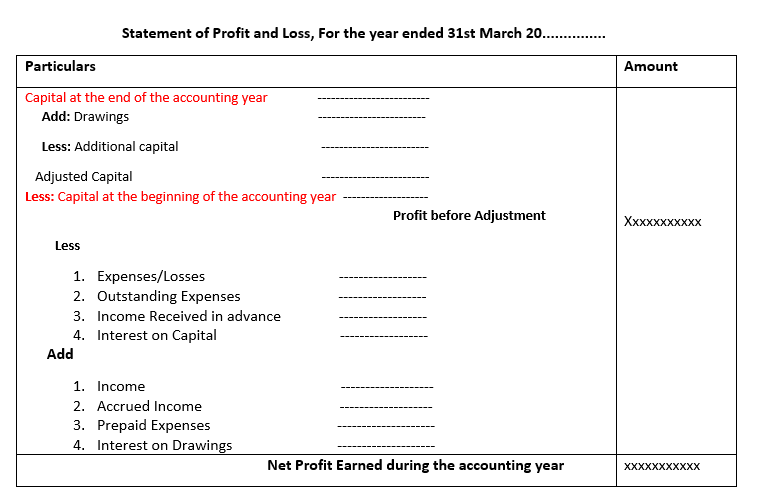

- Statement of Profit and Loss

(Calculation of profit by Net Worth Method or Statement of Affairs method)

Calculate Profit with the help of comparison of Opening Capital and Closing Capital, after making adjustments for Drawings, Additional Capital and other items. This statement is Statements of Profit and Loss.

Additional Information (Adjustments)

1) Additional Capital:

Amount of cash or assets in kind brought by the proprietor/partners, during the year.

2) Drawings:

Cash/goods/assets withdrawn by the proprietor/partners from the business for personal use, during the year.

3) Other Items:

Subtract Depreciation, Bad debts, Reserve for doubtful debt etc. from the profit to calculate the Net Profit. Similarly, Add some items to arrive at the net profit. (Check in the question, as You have done in Final Accounts under Double Entry System).

Proforma of Statement of Profit and Loss

Test Your Understanding - 1

Test Your Understanding - 2

Test Your Understanding - 3