Preparing BRS by Debit Credit Method

Steps for preparing Bank Reconciliation Statement:

First step:

After preparing the format given below, start with the given bank balance (as the case may be).

Second step:

Debit BRS in case of Short Debit/ Omitted Debit/ Excess Credit in Cash book /Passbook (as the case may be).

Third step:

Credit BRS in case of Short Credit/ Omitted Credit/ Excess Debit in Cash book /Passbook (as the case may be).

Fourth step:

Calculate the difference of both the sides and put that amount on the side having short total. Give the name of that side having short total to the bank balance as per the other book i.e. Cash book or Passbook (as the case may be).

Summary of Debit Credit Method of Preparing BRS

(a) Start with one bank balance,

(b) Dr. BRS if Cash book or Passbook has not been debited or wrongly credited.

(c) Cr. BRS if Cash book or Passbook has not been credited or wrongly debited.

(d) Calculate the difference, put it on shorter side and give the name of this shorter side to the bank balance of the other book.

Format of Bank Reconciliation Statement

| Sr. No. | Particulars | Dr. (₹) | Cr. (₹) |

|---|---|---|---|

| 1. | Bank Balance as per Cash Book/Passbook. | Xxx | (xxx) |

| 2. | Cheques drawn but not presented. | Xxx | |

| 3. | Cheques paid into bank but not credited. | Xxx | |

| 4. | Bank Charges. | Xxx | |

| 5. | Bank Balance as per Passbook/Cash Book. | (xxx) | xxx |

It is a custom to write Add/Less with the particulars, for that, you can write ‘Add’ the particulars having the amount on the side of the starting balance and ‘Less’ with the particulars having the amount on the opposite side.

The biggest advantage of Debit Credit Method

You don't have to change the treatment in case of different nature/types of Balance given as per Cash Book or Passbook.

Summary of entries in Bank Reconciliation Statement:

| Sr.No. | Particulars | Dr. (₹) | Cr. (₹) |

|---|---|---|---|

| 1. | Bank (favorable) balance as per Cash Book. | Xxx | |

| 2. | Unfavorable (overdraft) balance as per Passbook. | xxx | |

| 3. | Cheques issued but not presented for payment. | Xxx | |

| 4. | Cheques issued but dishonoured. | Xxx | |

| 5. | Cheques deposited but not recorded in cash book. | Xxx | |

| 6. | Interest on bank deposits not recorded in cash book. | Xxx | |

| 7. | Interest allowed by bank not recorded in cash book. | Xxx | |

| 8. | Bills collected by bank. | Xxx | |

| 9. | Direct deposits (payments by others) in bank. | Xxx | |

| 10. | Direct collection by the bank like dividend. | Xxx | |

| 11. | Short debit/omission of debit in cash book /passbook. | Xxx | |

| 12. | Excess credit in cash book/passbook. | Xxx | |

| 13. | Bank (favorable) balance as per Passbook. | Xxx | |

| 14. | Unfavorable (overdraft) balance as per Cash Book. | xxx | |

| 15. | Cheques deposited but not cleared/encashed/collected. | Xxx | |

| 16. | Cheques deposited but dishonoured. | Xxx | |

| 17. | Discounted bills receivable dishonoured. | Xxx | |

| 18. | Cheques received but could not be deposited into bank. | Xxx | |

| 19. | Direct payment by the bank. | Xxx | |

| 20. | Bank /incidental /collection charges debited by bank. | Xxx | |

| 21. | Interest charged by bank. | Xxx | |

| 22. | Short credit/omission of credit in cash book /pass book. | Xxx | |

| 23. | Excess debit in cash book/pass book. | Xxx |

Precautions

1. When entries as per cash book and pass book are compared for reconciliation, balances on the same date should be considered.

2. Only bank column of cash book is to be considered for this comparison with pass book.

Test Your Understanding of BRS:

Method of Preparing BRS

More Cases of Entries in BRS

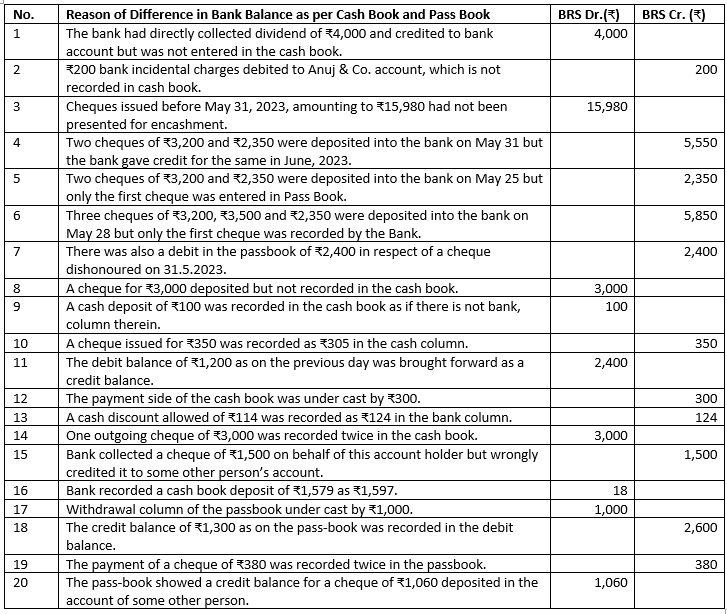

Following are some more cases where the difference was found in the bank balance as per Cash Book and as per Pass Book.

Bank Reconciliation Statement (BRS)

Learning Games and Activities in Accountancy – Class 11

FunwithAccountancy