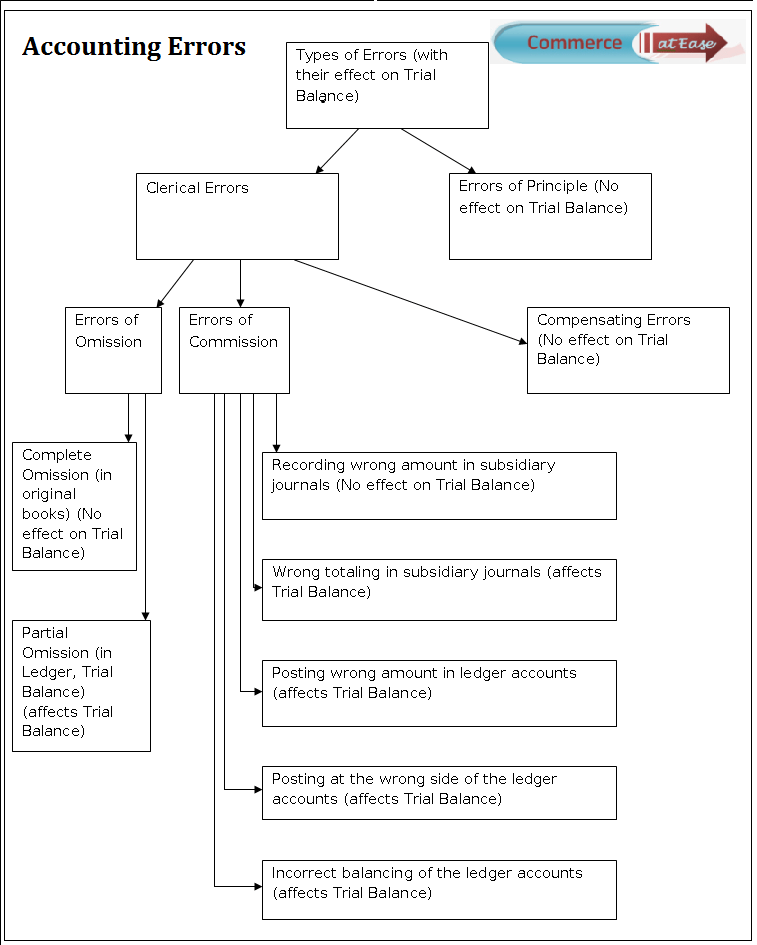

Types Of Accounting Errors

On the basis of Reasons of errors:

The errors are of basically following types:

(1) Errors of Principle:

These are mistakes due to lack of knowledge of accounting principles.

(2) Clerical errors:

These are mistakes due to carelessness, overlooking etc. Clerical errors can be:

(a) Errors of Commission:

These are mistakes due to wrong totaling, posting, wrong balancing, and wrong carry forward in the accounting books.

(b) Errors of Omission:

These are mistakes due to omission of entries in the subsidiary journals, omission of posting, omission of carry forward etc. The omission can be complete or partial affecting single side or both the sides of the Trial Balance.

(c) Compensating Errors:

These are mistakes that cancel mutually. One excess Debit cancels one excess Credit; one short Debit cancels one Short Credit and so on.

On the basis of their Effect on Trial Balance:

The errors can be classified into:

(a) Errors not affecting the Trial Balance.

1. In case of complete omission of entry i.e. from original books.

2. In case of error of principle.

3. In case of compensating errors.

4. In case of wrong amount in books of original entry.

5. Error of posting i.e. correct side, correct amount but in wrong account.

(b) Errors affecting the Trial Balance.

All other errors will be disclosed by trial balance as the trial balance will not tally. Following are such cases:

1. Errors of posting to wrong side of the same or another account.

2. Posting the wrong amount, to same or another account.

3. Posting the wrong amount and to wrong side, to the same or another account.

4. There can be errors of balancing the ledger account.

5. There can be errors in totaling of ledger accounts or sides of Trial Balance.

6. Some partial omission of posting can be there i.e. from journal to ledger or from ledger to Trial balance.

On the basis of their Effect on number of sides affected:

The errors can be classified into:

(1) Single sided errors.

Single sided errors affect only one side of the Trial Balance.

(2) Double sided errors.

Double sided errors affect both the sides of Trial Balance, by equal amount or unequal amounts.

Identify the Types of Errors: