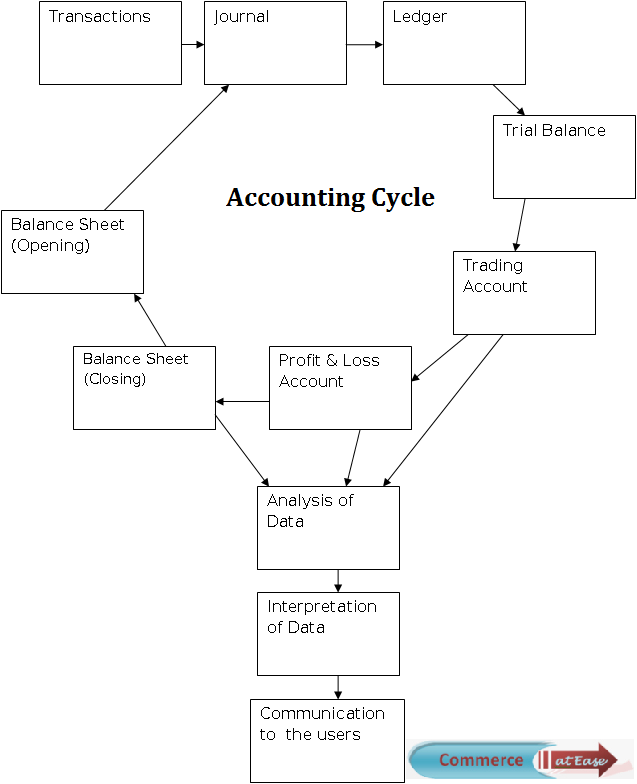

Accounting process starts with transactions that are recorded in waste book.

Then from there the transactions are recorded in the Journal, which is classified on the basis of similarity of transactions usually called subsidiary journals like; Purchases Day Book, Sales Day Book, Purchases Returns Book, Sales Returns Book, Bills Receivable Book, Bills Payable Book, Cash Book further taking the forms of simple cash book, double column cash book, triple column cash book, petty cash book, multi column cash book, etc. and Journal proper.

The next stage is, when entries passed in journal are further posted in Ledger. Ledger is set of accounts: real, personal as well as nominal accounts.

After posting all the journal entries to ledger, ledger accounts are balanced and from all the balances a summary statement known as Trial Balance is prepared to check the arithmetical accuracy of records.

Trial Balance is used to prepare the Final Accounts. From Trial Balance all the nominal accounts are taken to prepare Manufacturing account, Trading account and Profit and Loss account respectively as the case may be, and all the real and personal accounts are taken to prepare the Balance sheet.

Closing Balance Sheet of one accounting year becomes the Opening Balance Sheet of the next Accounting year. Then, next year transactions enter the accounting process and this cycle continues, making it Accounting Cycle.

Final accounts i.e. Trading Account, Profit and Loss Account and Balance Sheet are further analyzed with the help of accounting tools and techniques and then conclusions are drawn and then communicated to the interested parties for decision making.

CHART SHOWING ACCOUNTING PROCESS:

Accounting Process

This video explains the different Steps in the Process of Accounting.

▶ Watch this video on YouTube

Interactive Activity: Introduction to Accounting