Meaning of Controlling

It ensures that activities conform to the standards set in advance so that organizational goals are achieved.

Controlling means ensuring that activities in an organization are performed as per the plans. It also ensures that an organization's resources are being used effectively and efficiently for the achievement of predetermined goals.

Controlling function of a manager is a pervasive function.

It only completes one cycle of management process and improves planning in the next cycle.

Importance of Controlling

1. Accomplishing organizational goals:

It brings to light the deviations, if any, and indicates corrective action.

2. Judging accuracy of standards:

It helps to verify whether the standards set are accurate and objective.

3. Making efficient use of resources:

By exercising control, a manager seeks to reduce wastage and spoilage of resources.

4.Improving employee motivation:

A good control system ensures that employees know in advance what they are expected to do .

5. Ensuring order and discipline:

It helps to minimize dishonest behavior on the part of the employees by keeping a close check on their activities.

6. Facilitating coordination in action:

Controlling provides direction to all activities and efforts of each department and employee by predetermined standards which help in coordination.

Limitations of Controlling

1. Difficulty in setting quantitative standards.

2. Little control on external factors.

3. Resistance from employees.

4. Costly affair.

Relationship between Planning and Controlling

*Planning and controlling are inseparable twins of management.

*Standards of performance set in Planning serve as the basis of controlling.

*Planning without controlling is meaningless.

*Controlling is blind without planning.

*Planning is a prerequisite for controlling.

*Planning is an intellectual process of taking decisions, Controlling, checks whether decisions have been put into desired action.

* Planning is prescriptive whereas, controlling is evaluative.

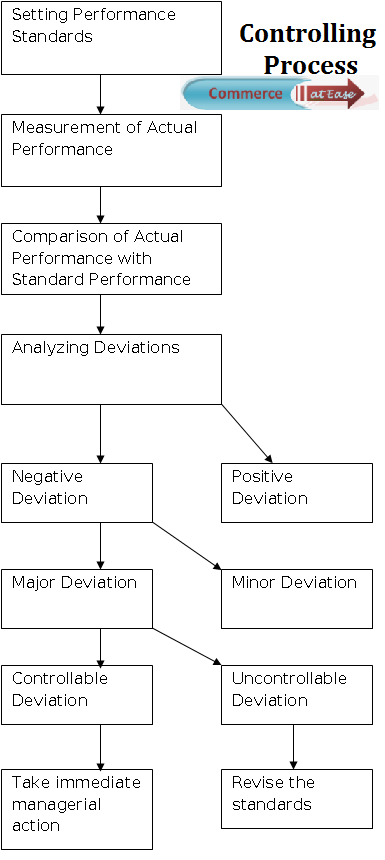

Steps in the Controlling Process

1. Setting Performance Standards:

Standards are the criteria against which actual performance would be measured.

Standards can be set in both quantitative as well as qualitative terms.

2. Measurement of Actual Performance:

There are several techniques for measurement of performance like personal observation, sample checking, performance reports, etc.

3. Comparing Actual Performance with Standards:

Such comparison will reveal the deviation between actual and desired results. Comparison becomes easier when standards are set in quantitative terms.

4. Analyzing Deviations:

Some deviation in performance can be expected in all activities. So, it is important to determine the acceptable range of deviations.

Critical Point Control:

Control should, focus on key result areas (KRAs) which are critical to the success of an organization.

Management by Exception:

An attempt to control everything results in controlling nothing.

5. Taking Corrective Action:

No corrective action is required when the deviations are within acceptable limits. But, when the deviations go beyond the acceptable range, especially in the important areas, it requires immediate managerial attention.

Test Your Understanding

Controlling – Keywords and Brief Notes

Budgetary Control

Meaning of Budgetary Control:

It is a technique of managerial control in which all operations are planned in advance in the form of budgets and actual results are compared with budgetary standards.

Budget:

It is a quantitative statement for a definite future period of time for the purpose of obtaining a given objective. It is also a statement which reflects the policy of that particular period.

Advantages of Budgeting

1. Budgeting helps in attainment of organizational objectives by focusing on specific and time-bound targets.

2. Budgeting enables employees to perform better by motivating them by fixing the standards against which their performance will be appraised.

3. Budgeting helps in optimum utilization of resources by allocating them according to the requirements of different departments.

4. Budgeting is also used for achieving coordination among different departments of an organization and highlights the interdependence between them.

5. It facilitates management by exception by stressing on those operations which deviate from budgeted standards in a significant way.